Covering the four weeks 02 February – 01 March

2025

-

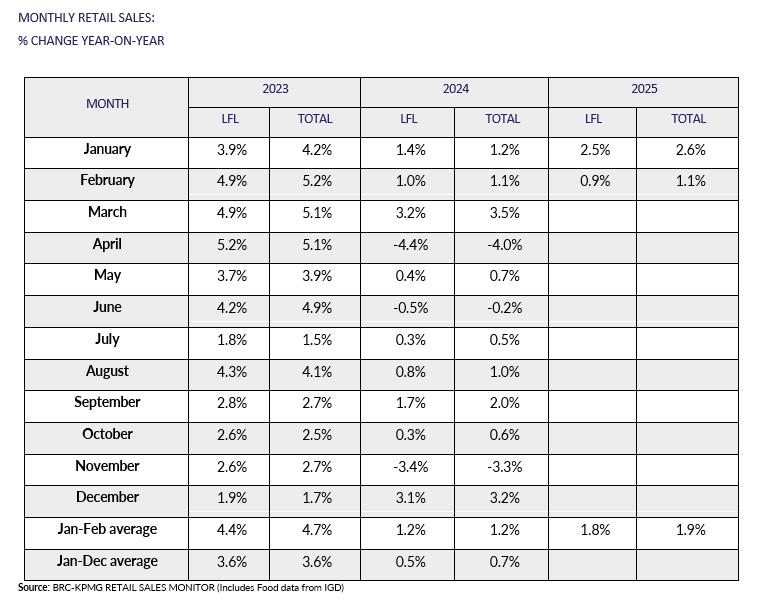

UK Total retail sales increased by 1.1% year

on year in February, against a growth of 1.1% in February 2024.

This was below the 3-month average growth of 2.4% and above the

12-month average growth of 0.8%.

-

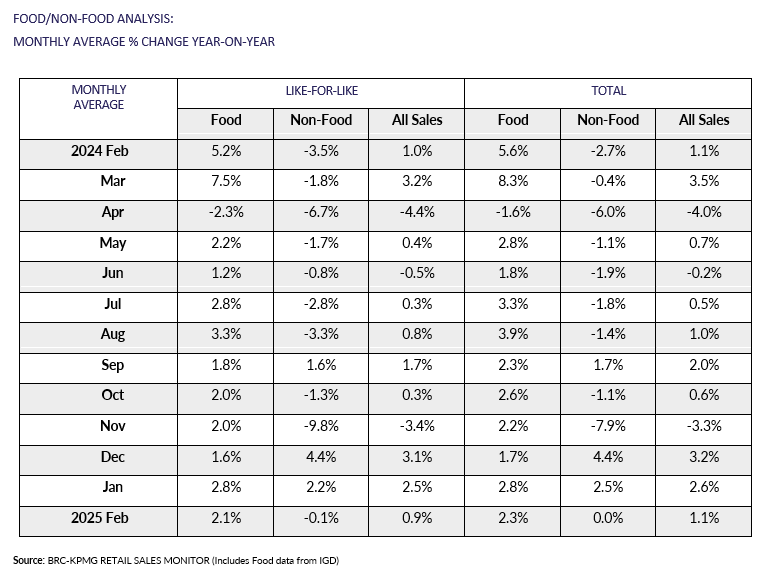

Food sales increased by 2.3% year on year in

February, against a growth of 5.6% in February 2024. This was

level with the 3-month average growth of 2.3% and below the

12-month average growth of 2.8%.

-

Non-Food sales were flat year on year in

February, against a decline of 2.7% in February 2024. This was

below the 3-month average growth of 2.5% and above the 12-month

average decline of 0.9%.

-

In-Store Non-Food sales decreased by 1.0% year

on year in February, against a decline of 1.8% in February

2024. This was below the 3-month average growth of 0.8% and

above the 12-month average decline of 1.7%.

-

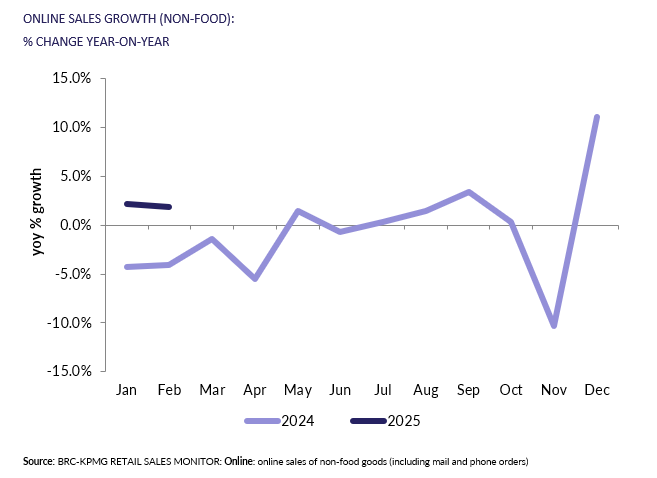

Online Non-Food sales increased by 1.9% year

on year in February, against a decline of 4.1% in February

2024. This was below the 3-month average growth of 5.3% and

above the 12-month average growth of 0.6%.

-

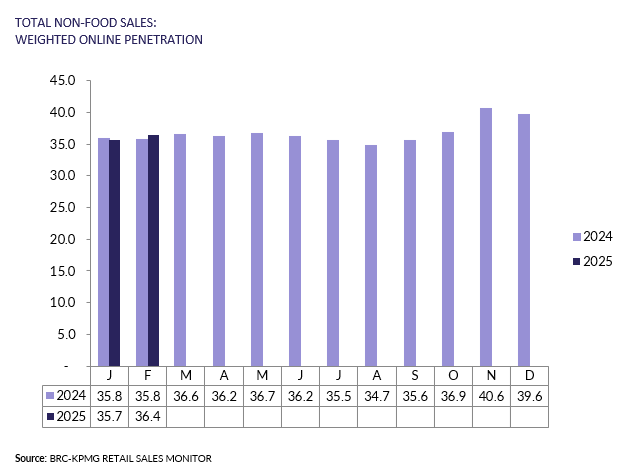

The online penetration rate (the proportion of

Non-Food items bought online) increased to 36.4% in February

from 35.8% in February 2024. This was below the 12-month

average of 36.7%.

Helen Dickinson OBE, Chief Executive

of the British Retail Consortium, said:

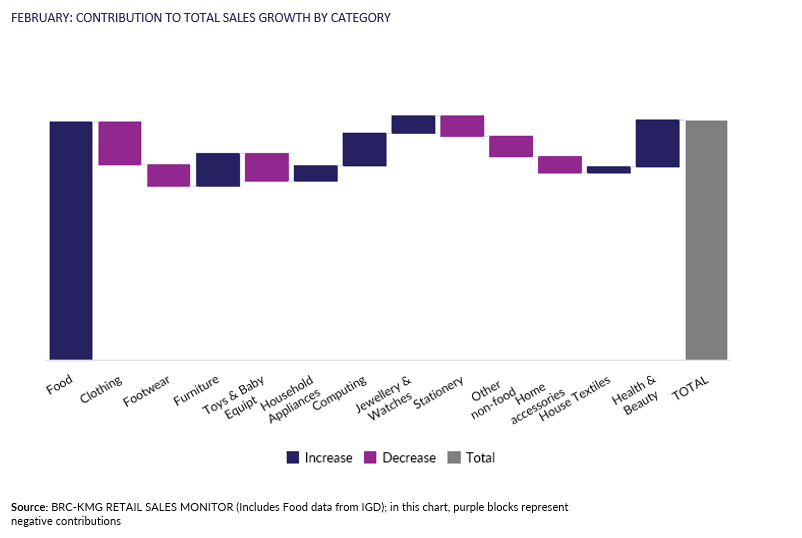

“Retail sales saw more modest growth in February. While sales

growth across non-food categories was generally muted, it was

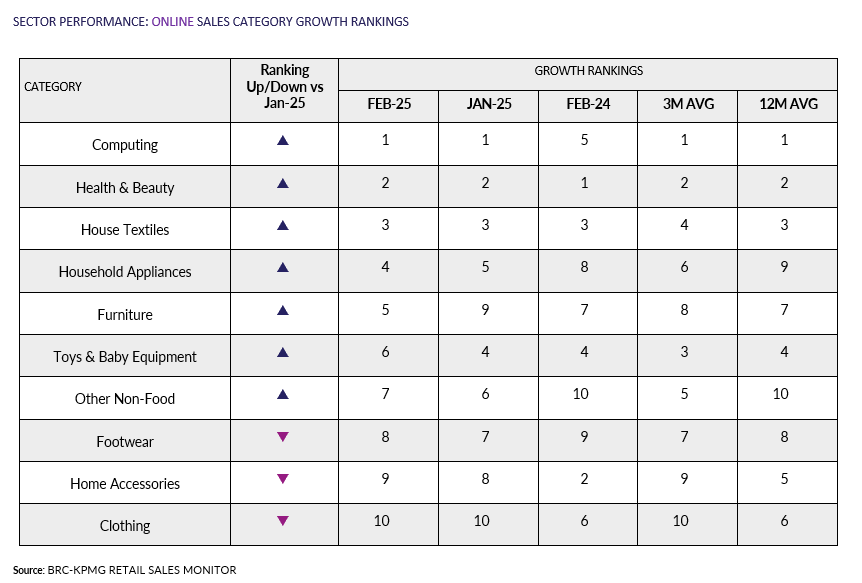

propped up by online purchases, particularly in computing and

electronics. Jewellery, watches and fragrance sold well thanks to

Valentine's Day, reversing declines seen last year, and furniture

also returned to growth. Fashion performed poorly due to the

gloomy weather throughout the month, but retailers are hopeful

the early March sunshine kickstarts spending on Spring and Summer

wardrobes.”

“This weak performance makes many retailers uneasy, especially as

they brace for £7bn of new costs from the Budget and packaging

levy in 2025, as well as the potential impact of the Employment

Rights Bill. The industry is already doing all it can to absorb

existing costs, but they will be left with little choice but to

increase prices or reduce investment in jobs and shops, or both.

The focus of the Employment Rights Bill should be on unscrupulous

employers but instead the industry faces ongoing uncertainty and

a trajectory that risks punishing responsible businesses who

provide valuable employment, particularly at entry level. It is

time for government to course correct to ensure investment and

growth are not undermined.”

Linda Ellett, UK Head of Consumer, Retail & Leisure,

KPMG, said:

“Consumers remain cautious with their spending and many are

continuing to prioritise saving, travel and experiences.

Nervousness about the economy is deferring other big ticket

purchasing, but occasions and offers are still tempting shoppers

into some impulsive spending. Valentine's, for example,

brought a jewellery sales boost to the high street, in what was

otherwise a flat month for in-store

buying.

“Online non-food sales growth is outpacing in-store and while

shops will always be a key part of many retailers' strategy -

rent, rates, and employment costs all must be factored in.

As we have seen already this year, firms are increasingly

scrutinising where best to be located and the implications of the

likes of recently announced employment cost rises. Online

shopping and the growth of social commerce has contributed to a

lowering of demand for some physical retail stores and boardrooms

will continue to keep a close eye on monthly footfall and sales

data as 2025 progresses.”

Food & Drink sector performance | Sarah Bradbury,

CEO, IGD, said:

"Despite upcoming cost challenges, shopper confidence rose to 2

(from -3 in January) due to wage growth and the impending rise in

the National Living Wage. Early February saw positive retail

value sales, likely from Valentine's promotions, but overall,

February's volume sales dipped. Shopper confidence is expected to

remain volatile in response to the external environment."

Source: ShopperVista research, 1000+ GB shoppers, February 2025.