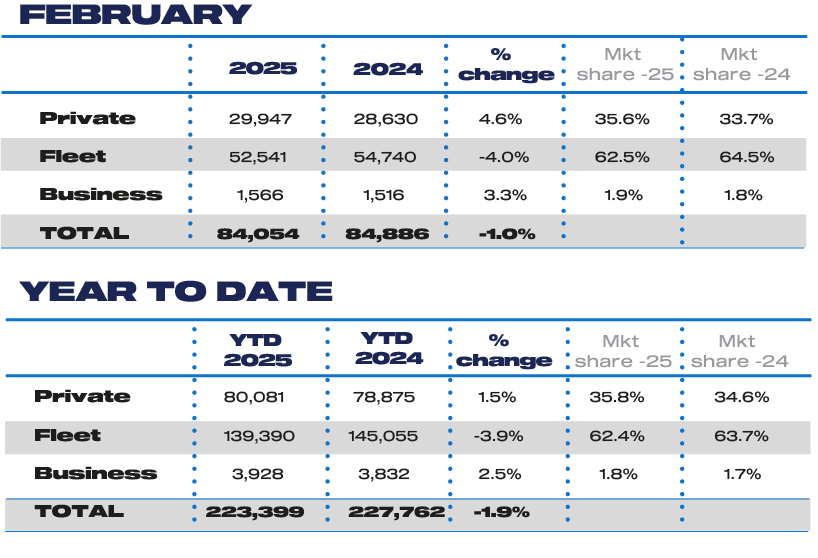

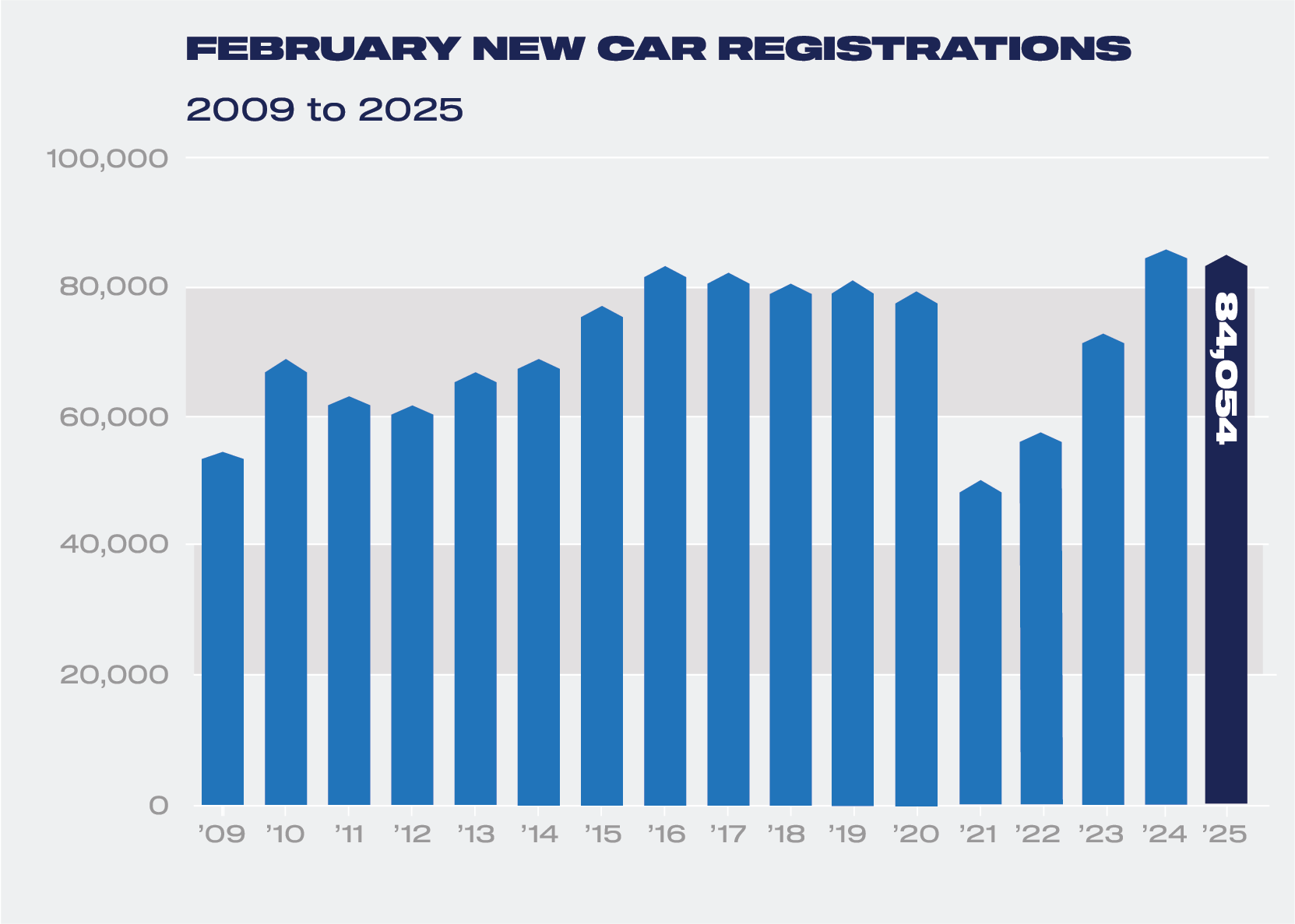

The UK new car market fell slightly in February, down -1.0% to

84,054 units, according to the latest figures from the Society of

Motor Manufacturers and Traders (SMMT).

In what is usually the smallest month of the year (accounting for

only around 4% of annual volumes), February was the fifth

consecutive month of decline, with a -4.0% reduction in fleet

registrations – which have driven previous market

growth. Private registrations rose by 4.6% to slightly increase

overall market share to 35.6%, while the much smaller business

sector rose by 3.3%.

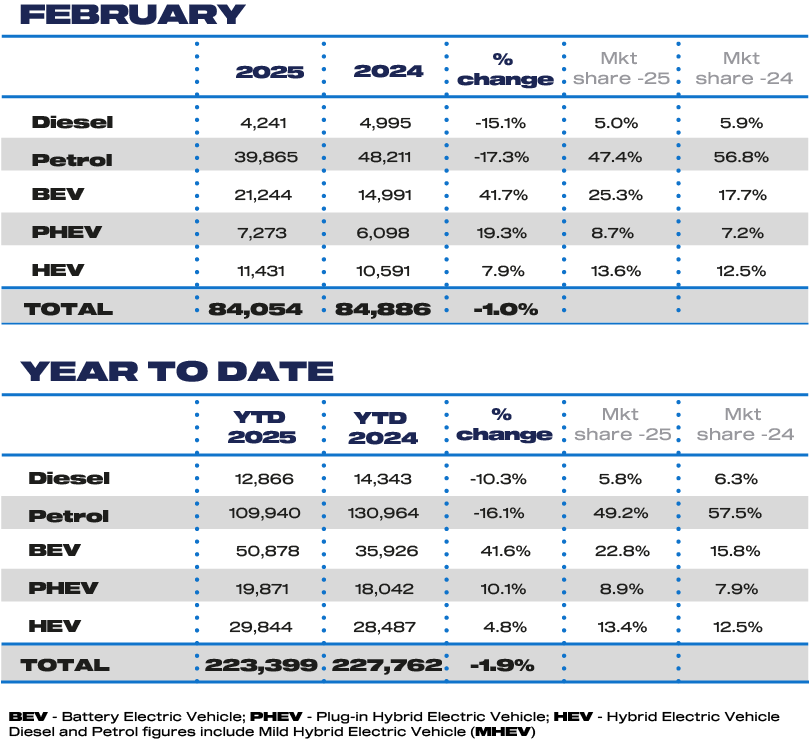

Electrified vehicle uptake continued to grow, with plug-in hybrid

vehicles (PHEVs) rising 19.3% and hybrid electric vehicles (HEVs)

up 7.9%. Battery electric vehicle (BEV) registrations

were up by 41.7% to 21,244 units, securing a 25.3% market

share compared with 17.7% a year ago. This dramatic increase

compared with the rest of the market was unsurprising

considering the forthcoming tax changes in April, which will see

many EV models subject to the vehicle excise duty expensive car

supplement (ECS) for the first time. This maintains the positive

trajectory but still falls short of the 28% target for 2025 and,

given February comes ahead of the March numberplate change, it is

always one of the smallest and most volatile months.

Next month is likely to see a further surge in EV uptake, as

buyers capitalise on the new '25 plate and take their last chance

to avoid the punitive ECS which, from 1 April will add £2,125

over six years to the cost of BEVs with a list price above

£40,000.1 Relative to the rest of the market, BEVs are

disproportionately affected as higher production costs meaning

the average BEV retails above the ECS threshold, a threshold

which remains unchanged since its introduction in

2017.2 The introduction of this measure also

risks disincentivising the used market as well as the new,

impeding a faster, fairer transition.

Manufacturers have already underwritten the transition to the

tune of more than £4.5 billion in discounts over the last year

alone – on top of the billions invested in developing and

bringing the vehicles to market. Such industry support is

unsustainable which is why the current ZEV Mandate must arrive at

measures which afford greater market flexibilities, incentivise

private purchases, and both encourage and facilitate a faster

rollout of charging infrastructure.

Mike Hawes, SMMT Chief Executive, said,

“Although February's figures show a subdued overall market, the

good news is that electric car uptake is increasing, albeit at

huge cost to manufacturers in terms of market support. It is

always dangerous, however, to draw conclusions from a single

month, especially one as small and volatile as February. With the

all-important March number plate change now upon us, and tax

changes taking effect in April that will, perversely, dissuade EV

purchases, we expect significant demand for these new products

next month - but, long term, EV consumers need carrots, not ever

more sticks.”

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Notes to editors

1 BEVs are currently exempt from all VED. From 1 April,

all BEVs will be subject to £10 VED in the first year of

ownership, followed by annual VED of £195, currently, in

years 2-6 (£975), for a total of £985. For BEVs more than

£40,000, an additional £425 is currently charged annually

in years 2-6 (£2,125) on top of standard VED, to give a

total of £3,110.

2 JATO sales weighted average BEV list price 2024:

£48,600

|